Earnings Review for PYPL, JKHY, Fiserv

|

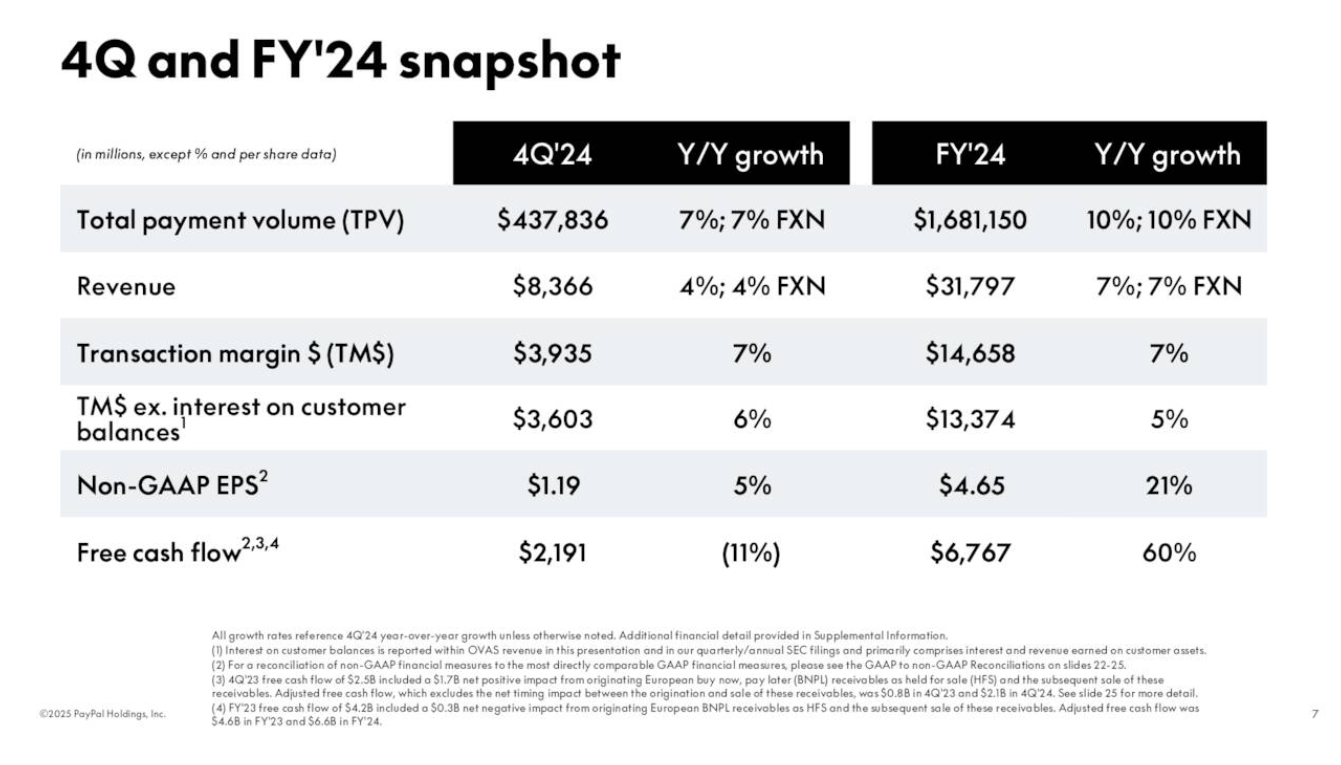

It has been interesting to watch financial software take off for the past few weeks. For the most part, fintech has been dead for two years. The capital markets were non-existent for the public fintech companies. But in the past few weeks, we’ve seen an uproar in fintech. All across the board, fintech stocks have gone up and to the right. The Trump Administration has been bullish for the industry. The obvious front has been for crypto, when President Trump nominated David Sacks as the Czar of Crypto and A.I. Sacks was the first Chief Operating Officer (COO) of PayPal. David’s nomination was very positive for the industry. PayPal earningsLet’s begin with PayPal. This is one stock that has been compounding returns for decades. I remember studying this company early on when Peter Thiel wrote his startup book, Zero to One. Peter was the co-founder and CEO of PayPal before it was acquired by eBay for $1.5 billion. When he first made PayPal’s first financial model, he realized it would take +10 years for the company to realize positive enterprise value. Well today, that $1.5 billion is worth $78 billion. If you look at the financial snapshot below, your eyes may look down at total payment volume and revenue. Both are moving in a positive direction. While I’m not an expert in payment processors here, the growth in transaction margins seems to be healthy.

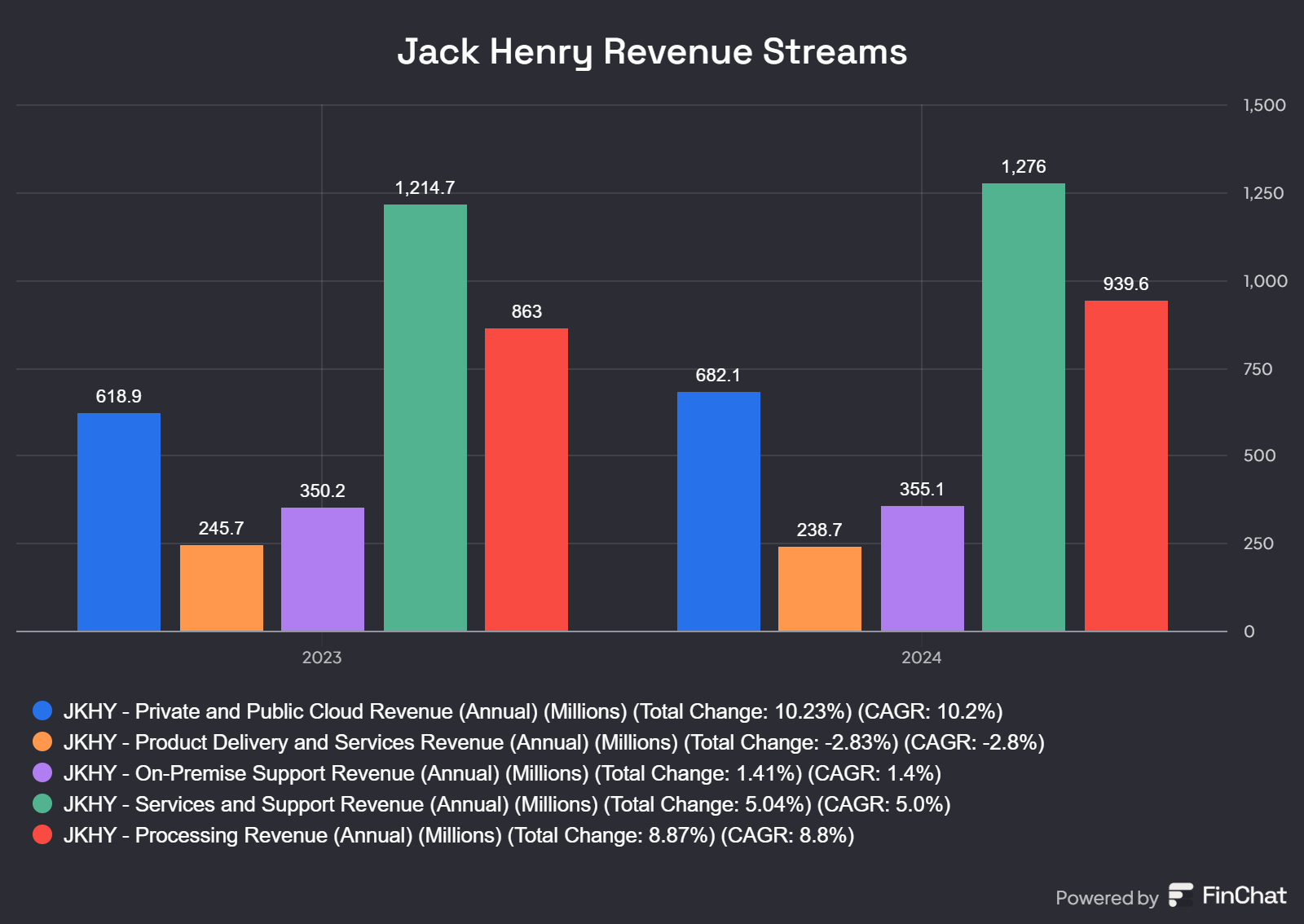

When I was first studying PayPal years ago, I learned that Peter Thiel and the gang worked very hard to make sure the company wasn’t labeled as a bank. PayPal was a major payment processor and held billions of dollars of customer reserves. But these weren’t checking accounts. They were account balances and PayPal was making money on the interest. You can see they still make money from these customer balances today. To the tune of $13 billion now. If you are thinking about investing in PayPal, I recommend focusing on the free cash flow numbers. Today free cash flow is growing 60%, which is significant when you realize they produce $31 billion in top-line revenue. Overall, I think the company will maintain its leadership and continue to be very profitable. PayPal is a stock worth looking into. Jack Henry & AssociatesIt’s unlikely you’ve ever seen the name. Personally this is a stock I’ve observed for years, but through the software M&A lens instead of financial software. Now from the name, it’s tough to know what Jack Henry the company does. Like PayPal, Jack Henry is a financial technology company but focuses on digital banking. Capitalizing on that one trend is why the stock has gone parabolic for two decades.

Jack Henry’s revenue comes from software and services. Most tech investors chase software businesses because of the high gross margins and premium valuations. However, if you work or invest in software, you will know that the real money comes from maintenance margin revenue. Which is the incremental dollars for updating software overtime. Constellation Software popularized this methodology when buying software companies.

Jack Henry is on my watchlist for several reasons. The primary being its ability to generate significant amounts of cash from operations. This company is a well oiled machine and averaging above the 20% return on equity I look for in companies.

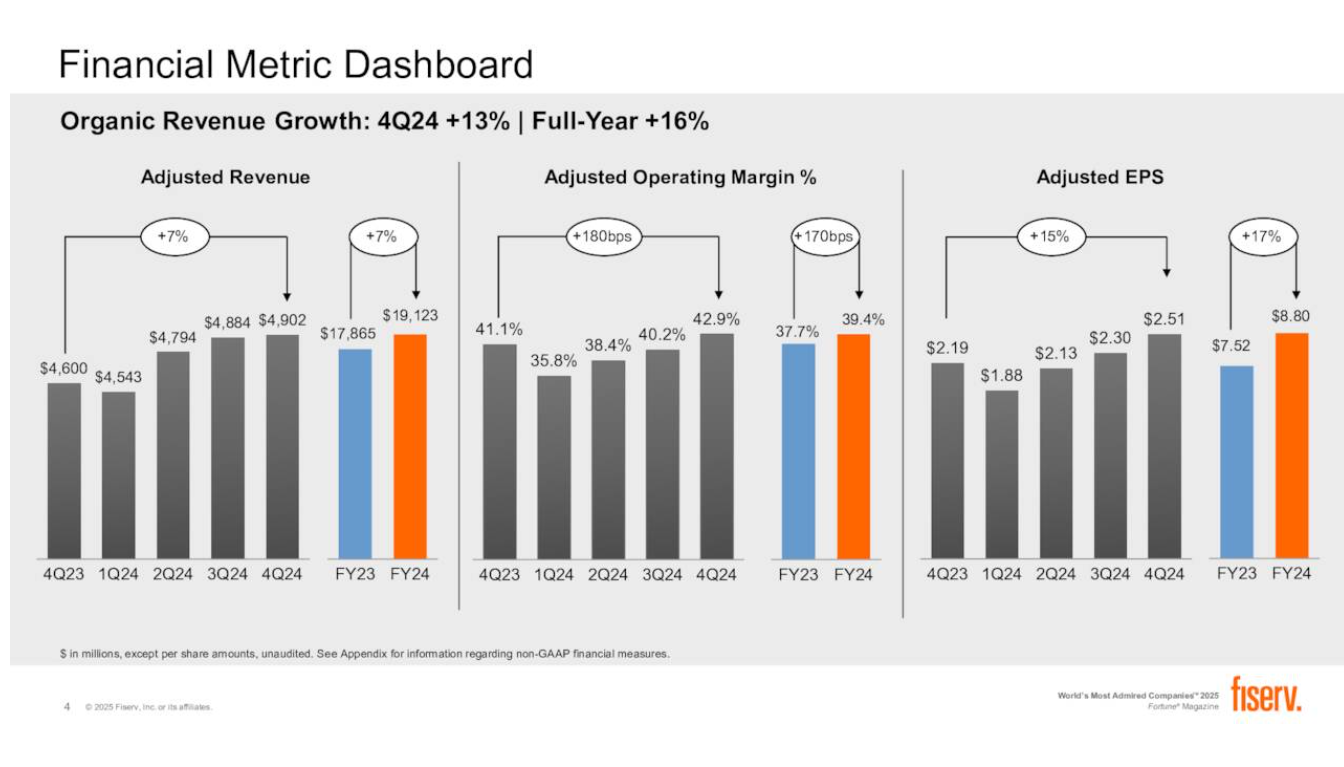

Since I’m revisiting this company, I need to spend more time analyzing their business model. This stock can very well be a core position in any portfolio, given how well it compounds capital over the long run. FiservI mentioned this company in December 2024 because of the Trump Administration. At the time, Frank Bisignano was the president and CEO of Fiserv and was nominated to be the commissioner of the Social Security Administration. This was the second fintech entrepreneur I watched be nominated for the Trump Administration. The first was Jared Isaacman, who is the founder and chairman of Shift4, another multi-billion dollar payment processor. But Fiserv is 16x larger than Shift4 with significant revenue streams. Like other payment processors, Fiserv makes a majority (81%) of its revenue from transaction services. This is a consistent and profitable revenue stream. And with enough operating leverage, these businesses can deliver significant profits with positive net retention.

Fiserv generates $19 billion in revenue with mid-teen profit margins. In the most recent quarter, they were able to deliver organic revenue growth through their three business lines. What impresses me the most is the size of Fiserv and how they are compounding capital.

Financial software is an exceptional business when it has operating leverage. Fiserv is a great example of one company that achieved these profits with organic growth.

|

Welcome to Golden Door

Learn about the latest technology investments here.

ADBE Return on Equity Analysis: Navigating the Digital Media Landscape A daily market insight into Adobe's financial performance, growth prospects, and competitive positioning. 6/10/2025 Daily Market Insights Your daily dose of market intelligence6/10/2025 Return on Equity Scorecard: ADBE Adobe (ADBE): A Creative Powerhouse in a Shifting Landscape Adobe (ADBE) remains a dominant player in the digital media and marketing solutions space, but recent performance reveals a nuanced picture. While...

Navigating Market Turbulence: A Daily Briefing Inflation, Rates, and Recession Risks: Expert Insights for Informed Investing 6/9/2025 Daily Market Insights Your daily dose of market intelligence6/9/2025 Executive Summary The market currently navigates a complex landscape characterized by persistent inflation, rising interest rates, and slowing economic growth, creating a challenging environment for investors. The Federal Reserve's hawkish stance to combat inflation, while necessary, increases...

Market Navigator: Daily Economic Briefing Navigating Inflation, Rate Hikes, and Market Volatility 6/4/2025 Daily Market Insights Your daily dose of market intelligence6/4/2025 Executive Summary The market is currently navigating a complex landscape characterized by persistent inflation, rising interest rates, and slowing economic growth, leading to increased volatility and investor uncertainty. While recent inflation data suggests a potential peak, the Federal Reserve remains committed to its...