Semiconductor Industry Analysis: Qualcomm, ARM, and Intel Earnings

|

Semiconductors are in the mid-stages of the investment cycle. Right now, the investors making the most money on semiconductor stocks have been in the game for multiple years. Of course this includes stocks like Nvidia, Intel, AMD and many more. If you are new to the industry, you will be surprised by how fragmented the landscape is. I’m not an expert in the industry but I have built PC computers by hand. Deciding between graphics cards for different video games was a hard and difficult decision. In the early 2000s, that decision probably cost only $500-$1,000. But today the compute power necessary to power artificial intelligence is off the charts. I’ve seen Nvidia's H100 GPUs range from $25,000 to $40,000 per unit. Well beyond the price of a typical Macbook. And that’s only the price of a GPU. You still need to spend quite a bit on training and software. So to help investors, I thought it would be good to cover a few semiconductor stocks. I’m not invested in these positions but might be over time. It’s always helpful to get a headstart if you want to build a multi-year position in any specific sector. Especially one like semiconductors which have many moving parts. My thesis here is simple. Semiconductors are in everything and the demand will continue to multiply. At first, these chips were used in microwaves and cars. But now see them in computers, phones, cars and eventually robots. Intelligence has no limit and invest in semiconductors is the beginning of that limit. QualcommYou’ve probably seen the name before but can’t remember where. Qualcomm is the wireless technology that is the backbone of all 3G, 4G, and 5G networks. Their name is synonymous with major phone brands like Apple and Samsung. They also happen to have a very profitable business model.

Now there’s no doubt this company has a significant moat. It has healthy margins and the ability to invest at even higher rates of returns. This compounds their competitive edge. So after cell phones, I think the next stage of mobile technology will be cars. We’re already seeing this happen with Tesla’s and Starlinks, thanks to Elon. However, wireless connectivity is not available in all vehicles yet.

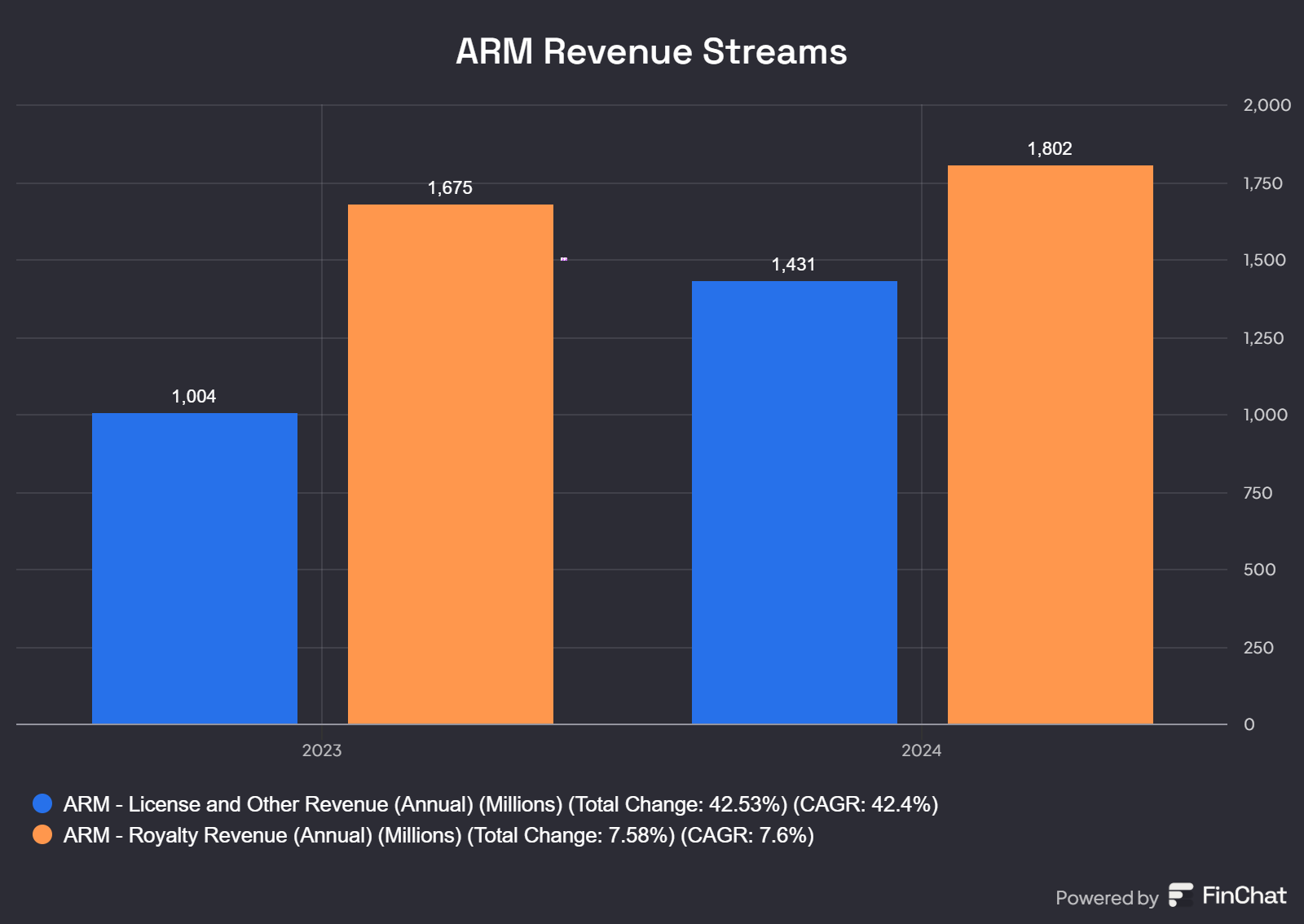

I think the next big breakthrough for this business for Qualcomm will be autonomous driving. There will be a tremendous amount of compute necessary in different components of every vehicle. The wireless communication bands will be powered by Qualcomm. That’s why their Automotive Revenue division is 61% this year so far. While the growth rate might slow down in the near-term, it doesn’t seem like the momentum will stop anytime soon. ARM HoldingsI’ve written about ARM several times on X because of their relationship with SoftBank. I first remember reading about this business in 2018-2019. This was a few years after Masayoshi Son and SoftBank made a bid to take ARM private at $32 billion. For context, ARM is worth $176 billion, so SoftBank made 5x his money on this deal. ARM was a massive win for the Vision Fund when it IPO’d in 2023. (if you weren’t aware, Masayoshi Son also offered Jensen to take Nvidia private in 2017. This would have been a double home-run for SoftBank and the Vision Fund.) Now ARM holdings is a very technical business. Their chips are used in Apple and Qualcomm architecture for smartphones. I think they have a 99% market share of smartphone CPU cores. Revenues are up 19% year-over-year, which includes royalties and licensing. Both are consistently growing and will probably continue for the time being.

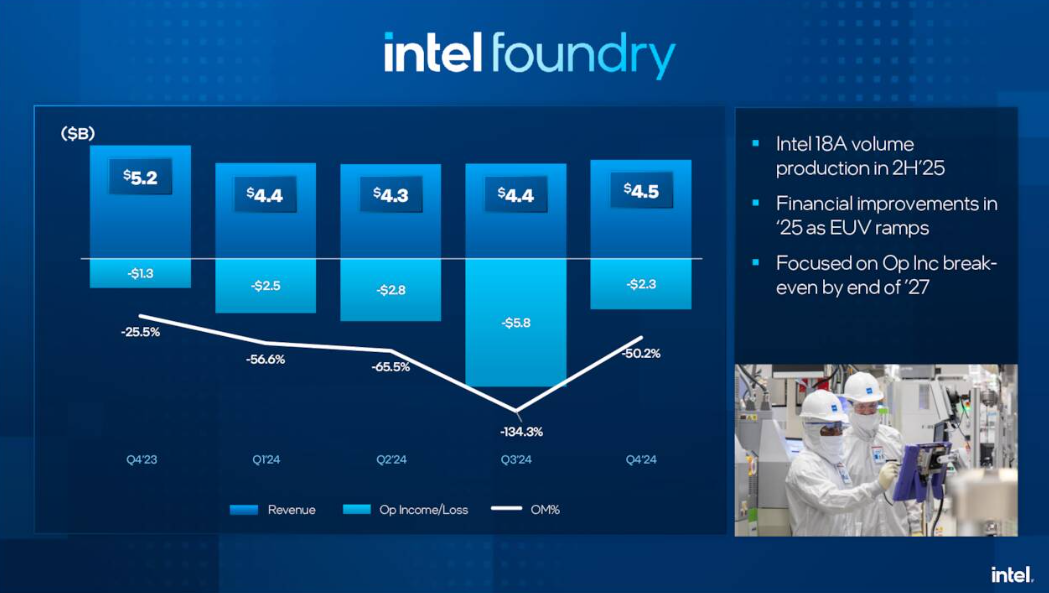

IntelAmerica’s first major semiconductor company is seeing revenues down 2%, year-over-year. The driver for this decline has been the Foundry business which dropped $17.5 billion. Given the success of Nvidia, Intel has reentered the conversation because they once led the semiconductor industry. The once-king is now down 54% in the past year but still a $83 billion business. Even though the CEO stepped down and the stock price is stumbling, Intel continues to have a resilient core business.

However there are some elements that are deteriorating. The biggest one continues to be the Foundry. I think Intel is feeling serious pressure from Taiwan, Singapore and South Korea. The CHIPs Act in the United States will not save them. The current rumors are Intel might need to spin-off the Foundry business, and private equity will be the buyer.

Overall, Intel is a good but deteriorating business. I wouldn’t be surprised if their market cap gets cut in half in the next 12-18 months. The market for CPUs is eroding and even I am personally looking to buy GPUs for my next computer. The power differential is too great and Intel simply doesn’t have the resources to compete anymore.

|

Welcome to Golden Door

Learn about the latest technology investments here.

The Rise of Crypto, Again In October, I last wrote about Coinbase’s progress before the U.S. Presidential election. It was significant on many fronts. Now it looks like the market is reviving and preparing for the next bull run. Let’s review the current state of the market. Crypto’s New Czar I’ve been following David Sacks for years. He’s a brilliant investor, founder and podcaster. I first learned about Sacks when he was building and selling Yammer. At the time, Microsoft buying Yammer for...

It has been interesting to watch financial software take off for the past few weeks. For the most part, fintech has been dead for two years. The capital markets were non-existent for the public fintech companies. But in the past few weeks, we’ve seen an uproar in fintech. All across the board, fintech stocks have gone up and to the right. The Trump Administration has been bullish for the industry. The obvious front has been for crypto, when President Trump nominated David Sacks as the Czar of...

The Semiconductor Trade War: Navigating Choppy Waters for Investors In the past two weeks, the global trade landscape has shifted and the economic tensions continue to rise. Now most investors are focused on tariffs and the rising cost of goods for the right reason. With the Trump Administration, a lot has happened on the front line of America. If you’re new to investing or unfamiliar with macroeconomics, trade wars look like uncharted territory. Your primary concern might be the rising cost...